The second ‘once-in-a-generation’ fossil shock in four years has put energy back on boardroom agenda.

Commercial and industrial (C&I) behind-the-meter (BTM) energy solutions have been quietly getting more compelling for years, but take up was slow.

The renewed focus, aided by surging AI data centre power demand and the proliferation of batteries, is catalysing accelerated C&I adoption.

Here we examine the causes and investment opportunities.

Long-term drivers

1. Economics: the value spread keeps widening

The core BTM solution remains solar. At its simplest, C&I solar competes with grid electricity. The economic case strengthens when the cost of grid power rises or becomes more volatile, and when the cost of self-generation falls. Both sides to this equation are moving in favour of C&I energy solutions.

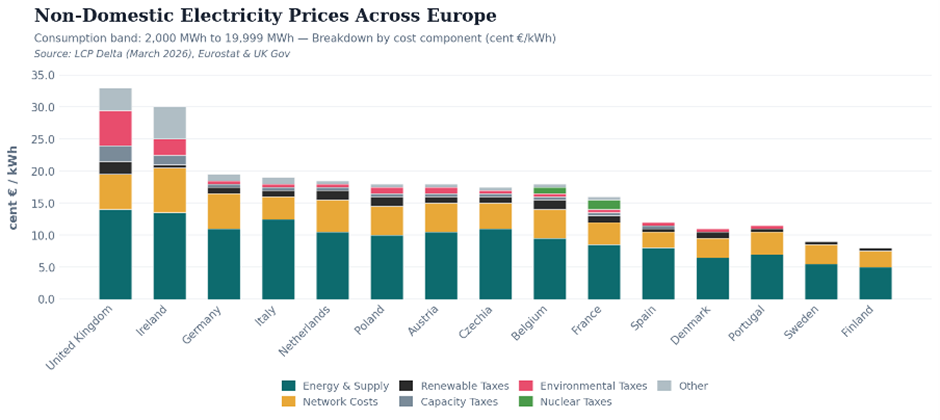

The cost of grid power for C&I customers combines wholesale power prices plus network costs and levies that can be ~50% of the total bill in many European countries, and up to 60% in the UK.

Wholesale prices, while a long way below 2022 peaks, remain structurally higher and more volatile than pre-Ukraine norms. Following the more recent crisis in Iran, power prices in countries where gas remains a key part of the generation mix (UK, Germany, Italy) have increased a further 10-20%.

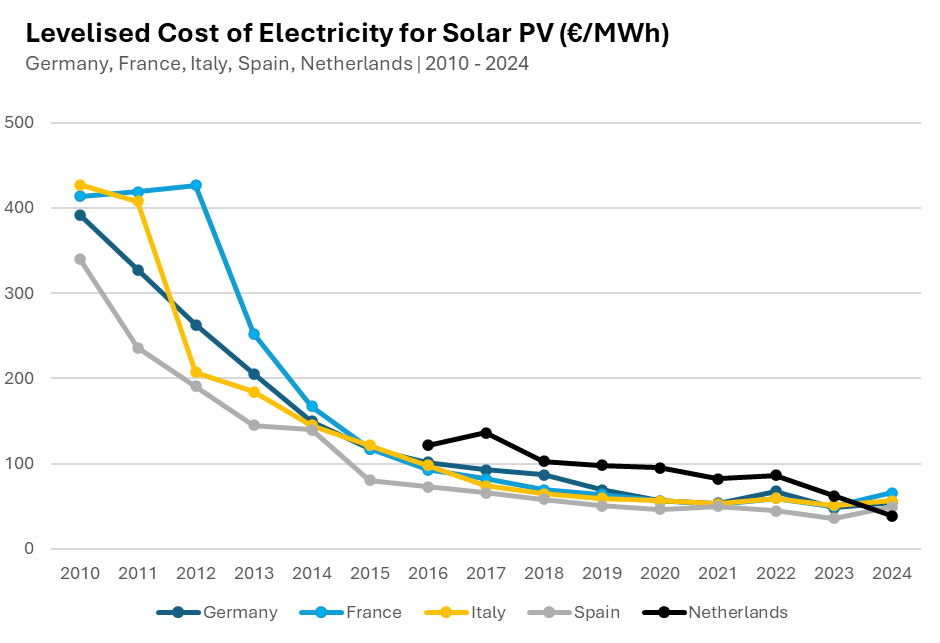

Set against this, the 90% decline in solar module costs has driven the levelised cost of electricity (LCOE) for BTM solar well below the cost of grid power for C&I customers.

Source: Ember IRENA Renewable Power Generation Costs in 2024

2. Converging tailwinds

Supporting the improving value proposition are other long-term factors:

So why now?

The surge in C&I energy activity post Ukraine has long since subsided. This masked underlying improvements in the proposition’s fundamentals. A catalyst was needed:

Opportunities for investors

1. Infrastructure: de-risked, scalable capital deployment

Where FTM grid-scale projects face transformer queues, connection delays, declining capture rates and merchant revenue uncertainty, C&I BTM sidesteps most of these. BTM can be built and energised in months. Infra capital, sated on grid delays, sees the merit.

The traditional objections to C&I – small project sizes, high customer acquisition costs, slow corporate decision-making – are being addressed.

Project sizes are growing, both through adding multiple technologies behind the meter (e.g. BESS) and through the growth of multi-MW ground-mounted solar projects that are connected directly to industrial customers (including data centres) by private wire.

Pipelines are once again growing and customer acquisition costs coming down. Regional variations matter – adoption will be greatest in countries with high grid power costs and most exposed to gas price volatility (UK, Germany, Italy).

We expect accelerated infrastructure investment activity and consolidation, both from existing platforms backed by the likes of Ardian, Antin, Brookfield, Octopus and KKR, and from new entrants.

2. Services: complexity creates value

The coming wave of infrastructure investment into C&I projects will also boost related services companies.

As systems become more sophisticated, the value chain is expanding. C&I deployments increasingly involve solar PV, battery storage, EV charging and energy management systems.

Engineering, EPC and O&M firms capable of integrating these technologies with building management platforms, and the skilled individuals they employ, are scarce and in growing demand.

We expect that private equity investors will focus in this area, attracted by the long-term market drivers and scarcity of skilled firms / individuals, echoing the characteristics that fuelled the recent high level of investment activity in Independent Connections Providers (ICPs).

3. Technology: software, flexibility and electrification

The next layer of value sits in optimisation. The combination of distributed generation, storage and flexible load creates a more dynamic energy system that requires active management.

Energy management software, demand-side response (DSR) platforms and virtual power plants (VPPs) will expand as will time of use tariffs. AI and advanced analytics will increasingly be used to optimise real-time energy flows, maximise self-consumption and participate in flexibility markets.

Adoption had been slow and breakeven elusive, but faster growth is making VC-backed firms such as GridBeyond, Capalo AI, iWell and Frequenz attractive acquisition targets.

A parallel opportunity exists in electrification hardware technologies including heat pumps, electric boilers and thermal energy storage. Whilst electricity prices have stabilised somewhat, gas prices remain elevated. This creates a favourable environment for electrified heating solutions and the attendant opportunity to store and flex solar energy as heat.

In effect, the C&I energy transition is expanding beyond power into heat, broadening the addressable market.

Conclusion

The European C&I energy market is entering a more buoyant phase.

Structural factors like improving economics, financing solutions and supportive regulation has created a compelling long-term case, but the urgency has been missing.

The impetus from high gas prices is proving the catalyst for widespread adoption.

For investors, the opportunity spans infrastructure, services and technology. There is renewed growth, unconstrained by grid bottlenecks and increasingly aligned with corporate strategy, supported by a stronger fundamental value proposition. Further upsides will come from scale and decreasing costs of capital, supply chain efficiencies and additional technology-enabled revenues e.g. VPP, DSR.

This is not a gold rush, this is a market quietly becoming indispensable. We expect that investments made now will benefit from compelling exit options in the years to come.