Despite the UK imminently awarding Long Duration Energy Storage [LDES] contracts at roughly four times the volumes of Italy’s MACSE round 1, anticipation is low. This overlooks supply chain and revenue consequences which could impact all UK BESS.

LDES defined

‘Shorter than a cricket match’ is not everyone’s definition of Long Duration. ‘The time between UK energy policy announcements and their delivery’ probably is. However we do not use duration: we define LDES by its purchasing mechanism – the salient parameter for project investors. The UK’s LDES scheme covers projects >8 hours, whereas Ireland and Italy settled at >4 hours. The technologies are generally familiar but deployed under new contracting models and configurations. LDES is typically just a more infra-aligned incarnation of batteries: long asset lives, significant capex, bankable contracts and inflation adjustments.

UK Cap and Floor

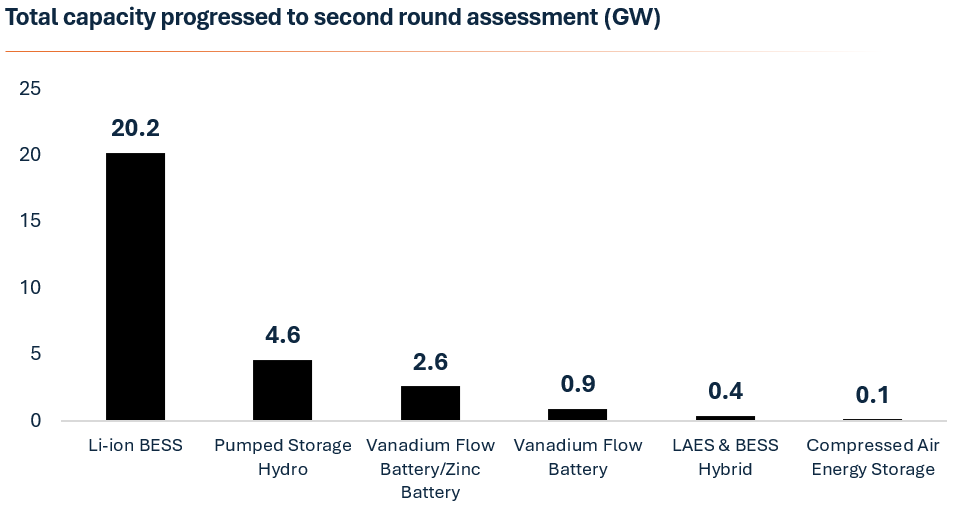

The biggest live scheme is now the UK (40 GWh vs MACSE 10 GWh). The British government intends to purchase 2.7-7.7 GW of LDES (minimum 8 hours), coming online in 2030, typically with 25 year cap-and-floor contracts. These will be selected from nearly 30 GW of pre-screened projects (implyin. Ofgem aims to honour ‘technology-neutral’, and ‘diversity of technologies’, but the fact is that only Li-ion gets reliably built in this time, so Li-ion dominates the shortlist: 70% of capacity.

Startling context

Work the maths on this, and the capex is startling. A volumetric mid point of Ofgem’s target is 5 GW: at least 40 GWh at 8 hrs. If each MW costs £1.5m at 8 hours (£190k/MWh), then mid-case volumes imply at least £7.5bn of investment. This spending is concentrated in three years: 2027-29. That is £2.5bn p.a – an astonishing sum, with serious implications. For context, Opus estimates this exceeds the UK’s total annual grid scale BESS investment in 2023, or even 2024.

Project Finance

Project Finance will fund a higher share of capital costs for LDES, rendering it significantly less equity intensive than shorter duration BESS, but the point stands: this is a material opportunity for grid infrastructure investors, and a material demand on UK supply chains.

Timings

Ofgem’s initial decisions on selected projects are due in April, with final awards due in “summer”. Few fortunes are made by betting on UK regulatory timetables being met, but we anticipate imminent activity as successful bidders rush to deliver £2.5bn pa of investment (financing, supply chain, EPC) to get projects online before 2030 and ahead of 3 year transformer delivery times.

Returns and Risk

These LDES contracts could excite a UK battery market historically reliant on merchant revenues. If we see floor equity returns above 6%, capital will flow. As a result, says Chris Matson at LCP Delta, “many BESS developers expanded projects that would have otherwise been 2 or 4 hours to meet the 8-hour threshold.”

But we’ve been here before, with simplistic expectations confounded by competition. The risk is of MACSE-type black swan outcomes. This could relate to the synergistic upstream to generation projects, the residual value of grid connections, deferred liabilities or another matter. Any might cause projects to be bid below standalone economic thresholds. Of course, these are far-fetched, but so was October’s MACSE outcome. So we are not yet ready to assume it’s a gold rush for equity investors, and are mindful that floor returns could prove disappointingly low.

Impacts

Typically with a gold rush, the money is made selling ‘picks and shovels’, and this scale of investment may strain supply chains, impacting availability, cost and timelines from project financiers, transformer OEMs, BoP contractors, EPCs, ICPs and DNO TPWs [third party works]. Current 3 year lead times for transformers will ensure many capital formation transactions are accelerated into 2027.

Worse, this large 40 GWh LDES deployment rush coincides with the imminent surge in shorter duration BESS deployment from TMO-4 Gate 2 delayed short-duration BESS assets. This is a potent cocktail for market tightness, cost pressures, and heightened execution risks. Some regions, notably Scotland which has a high concentration of LDES, may see concentrated local effects. There is general confidence the supply chain can handle this demand, but it’s a challenge.

BESS returns

Even assuming zero delivery and capex impacts, LDES will impact BESS returns. Zenobe argues that “by allowing subsidised LDES assets to compete directly with unsubsidised BESS in markets like balancing, response and capacity, the [LDES] policy could distort pricing and bidding behaviour, reducing the competitiveness of battery storage”. This is not wrong. 40 GWh of LDES assets will need to compete in the same arbitrage and ancillary revenue stacks, potentially depressing returns. LCP estimate LDES awards will knock 200 bps from BESS returns, creating a five year UK BESS investment hiatus from 2030. Other consultants see greater separation in the markets in which they compete, concluding the impact will be half that, but it will materialise.

Who wins?

These concerns are not endemic to LDES, they are a bug in British implementation. We can’t yet know how attractive UK cap and floor contracts will prove. Nor do we know which projects will be awarded, but the published shortlist reveals the charge is being led by NatPower (9.5 GW across 10 projects), DIF’s Field (1.6 GW across 5 projects), and Innova (1.6 GW across 4 projects). Contract wins could exceed current funding capability: so anticipate asset M&A as well as equity rounds following the final awards.

If the second round of LDES moves beyond 8 hours, we may see

A European phenomenon

Like BESS and syncons, the LDES opportunity too should spill out across Europe, and implementation there may be smoother. Italy used MACSE to deliver LDES. Ireland has started too (200 MW of 4 hour duration), and others will follow, for three reasons:

Just now, LDES may be as oddly British as treating emergencies with a cup of tea, but some form will become common across Europe soon: decarbonisation goals require it. The current form is merely a first step on this path. In forms longer than 8 hours, we may see real competition emerge to gas, perhaps through other molecular forms of storage. So don’t pre-judge the evolution of LDES based on current results.

Conclusions

Imminent UK LDES contract awards in the next 4-12 weeks will concentrate minds on LDES’ rewards, but also the risks. The scale of implied investment in the UK is being overlooked: it dwarfs recent UK BESS investment. It may pose a significant opportunity for winners, and for the BESS supply chain, but it brings risks, for LDES winners and for planned Gate 2 projects: 1) to timelines, 2) to their actual capex costs and achieved returns, 3) to broader project finance availability, and 4) to post 2030 revenues. It is currently a form of contracting Li-ion and pumped storage, but this may change as durations extend.

Stay tuned.